Social Security’s Math No One Wants to Face

“Bonne chance, mes enfants.”

For most Americans, Social Security feels like a simple bargain: you pay in during your working years, and the government sends you a check in retirement. Politicians in both parties have reinforced that impression for decades, assuring voters that their benefits are “earned” and that the program is safely tucked away in a “trust fund.” Last week’s Social Security Trustees report should have shattered that complacency, warning that the main retirement trust fund will be unable to pay full benefits within a few years under current law. Once you understand how Social Security is actually financed—and how Congress has used it to paper over wider deficits—it becomes clear why fixing it will require political courage that Washington has so far been unwilling to show.

The public has been so badly misled by politicians about how Social Security works that a real solution may be nearly impossible. First of all, Social Security is already running a cash-flow deficit, and we are borrowing roughly $160 billion this year to make up the difference—on top of everything else Washington is already financing with debt.

Second, the “trust fund” is made up of Treasury bonds, not taxpayer savings. When Social Security was running a surplus—that is, payroll taxes exceeded benefits—Congress used the surplus to reduce the deficit at the time; in exchange, the government credited Social Security with Treasury securities. Economically, that’s an internal IOU, but legally and financially, those bonds are real obligations of the Treasury.

In effect, this shifted costs over time—reducing deficits then while creating obligations that must be financed now. Given current fiscal conditions, that means the government will have to borrow even more to redeem the Treasury bonds in the trust fund and keep benefits flowing.

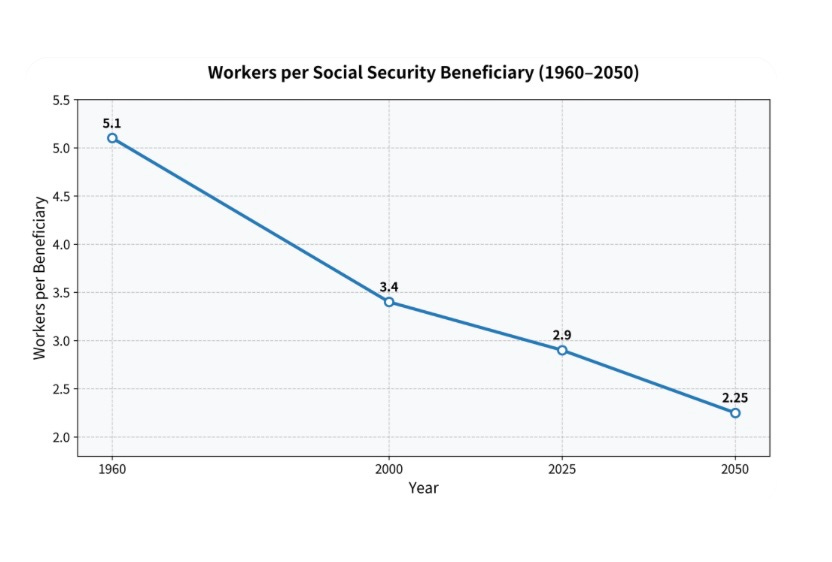

Third—and sorry to have to tell you this—there are not, nor have there ever been, individual savings accounts that your payroll taxes were paid into. Your payroll taxes have been used to pay the benefits of existing retirees. What is happening now is that benefits exceed the taxes paid, and this will only get worse as the population of working-age adults shrinks relative to the population of benefit-receiving seniors. Current law promises specific benefits, but it does not guarantee that your contributions were ever saved in a personal account. There is no mythical savings account that you have been putting money into.

So, what do we do? The government has been paying benefits using Treasury bonds held in the trust fund. Social Security’s shortfall is covered by redeeming those trust fund bonds. That redemption requires the Treasury to obtain cash—through taxes, spending cuts, or borrowing—which affects the unified federal deficit. According to the Social Security Trustees’ recent report, the bonds in the main Social Security retirement trust fund will be exhausted by 2032. In that year, the only money payable will be what workers pay into the system, and that will be only about 78 percent of what the law promised.

But who are we kidding? In theory, Congress could simply reduce Social Security benefits to 78 percent of what was promised. If you think that will happen, I have a bridge in Brooklyn I would like to sell you. Congress could raise payroll taxes, push back the retirement date for future retirees, or remove the income caps for FICA taxes, but all three would be politically unpopular. It could enact major reforms, as President George Bush proposed in 2005 and as many countries, such as Sweden, have already done—for instance, by shifting part of the system toward individually owned, market-invested accounts—but that was also politically unpopular.

So what will our Congress do? Regardless of which party is in power, it will borrow money to cover the difference between payroll taxes and the benefits that must be paid. The only real change will be explicit: Social Security benefits, above and beyond what is funded by the payroll tax, will be paid directly from general revenues. But as we’ve discussed, it has effectively been doing that already—using an accounting distinction that obscures the underlying fiscal reality. The Treasury “cashes out” bonds in the trust fund with money from the general budget and treats that as a separate transaction.

What does that mean? It means our budget deficit and national debt will balloon even further. Interest on the national debt already exceeds $1 trillion. As the trust fund is exhausted, Social Security will place increasing pressure on the rest of the federal budget—requiring higher taxes, more borrowing, or cuts elsewhere. Over time, that means higher interest costs, reduced fiscal flexibility, and a greater risk that markets begin to question Washington’s ability to manage its obligations.

So the economic stability of our children’s future depends on Congress making unpopular decisions to fix Social Security and other entitlement programs. Congress is unlikely to make those tough decisions—heck, it can’t even consistently make the tough decisions needed to manage our annual appropriation bills, much less future budgets.

In other words, “Bonne chance, mes enfants.” *

*When you have bad news, it is always better to say it in another language. Latin also works. Italics help.

A great explainer of how the OASDI (Old-Age, Survivors, and Disability Insurance) fund works. I wrote something similar and much longer for one of those "franked" mailers from my then-boss Rep. John Hiler's congressional office, where I was the press secretary, trying to sell our Indiana Third District constituents on the 1983 Social Security reform bill. Despite so much ink being spilled over the years, most people still don't understand it, and no one in Congress, and certainly not the President, will touch it, except to race towards insolvency faster, as they did in 2022 with the misnamed "Social Security Fairness Act," a sop to long-serving mostly state and local public employees. There are good fixes available, but it is getting late, and it's already too late for some to avoid the pain involved with any of them. Sadly, I fear you are right - Congress will just borrow from our children and grandchildren.

“… there are, nor have there ever been, individual savings…”

You left out the “not” after the word “are”.

Kinda important for the (correct) claim you are trying to make. 😏